Still Time to Save on Taxes This Year: Retirement Contributions for Therapists

As the end of the tax year approaches, many private practice owners are wondering: is there anything I can do now to lower my tax bill?

Good news—yes, there is. If you’ve got extra income this quarter or simply want to make smart financial moves before year-end, reviewing your retirement contributions is a great place to start. A few small steps before December 31 could mean serious tax savings in April.

Why It Matters

Retirement contributions can lower your taxable income for the year

You’re investing in your future while reducing your current tax bill

These accounts offer flexibility—some let you contribute up to the tax deadline in April

For official contribution limits and deadlines, you can review the IRS guidelines here.

Already Have a Retirement Account?

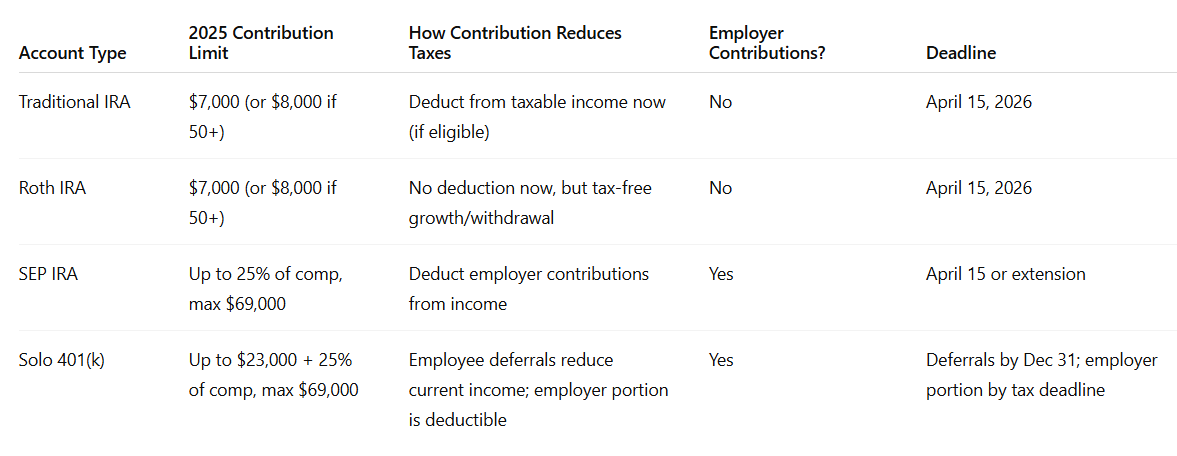

Here’s how much you can contribute before the year ends and how each type can lower your taxes:

Tip: Planning to open a Solo 401(k)? It must be established by December 31 to contribute for 2025.

Don’t Have a Retirement Plan Yet?

Here are some common options for therapists—and how to choose:

Solo Practice, earning under $100K?

→ Open a Traditional or Roth IRA (quick to set up, low maintenance)

Solo Practice, earning over $100K?

→ Consider a SEP IRA or Solo 401(k) to maximize your deduction

Group Practice Owner (with employees)?

→ Look into a SIMPLE IRA or 401(k) to stay compliant and attract talent

If you’re planning to contribute this year, don’t wait.

Some plans need to be set up by December 31 to count—check your options today.

Disclaimer: This post is for informational purposes only and should not be considered tax, legal, or investment advice. Always consult with a qualified tax advisor or financial planner before making decisions about retirement contributions. For official contribution limits and rules, visit the IRS Retirement Plans webpage.